Becoming a CPA is one of the most rewarding things you can do for your professional career. The process is challenging, but it’s completely worth it. The first step towards your goal is taking the CPA exam.

Becoming a CPA is one of the most rewarding things you can do for your professional career. The process is challenging, but it’s completely worth it. The first step towards your goal is taking the CPA exam.

The CPA exam consists of the following four sections:

- Auditing and Attestation (AUD)

- Business Environment and Concepts (BEC)

- Financial Accounting and Reporting (FAR)

- Regulation (REG)

Each of these exam parts is tailored to assess the competence levels of the candidates and their ability to execute basic and complex accounting tasks. The examination is usually set by the American Institute of Certified Public Accountants (AICPA) and is usually similar for all candidates sitting for it at any specific exam period. There may be other distinct requirements that may be set by the accounting board or the authority in specific states.

Before you even consider enrolling for CPA, it is critical to understand that you will only be awarded the credential and the powers to use the elite title of CPA after passing all the four sections. There is an 18-month rolling window that stipulates that the candidate must complete all the four sections of CPA within 18 months.

What this means is that, after passing the first section of the exam, in this case auditing and attestation (AUD), you must strive to complete the remaining three sections within 18 months. In case you fail to comply with the 18-months rule, the results of the first section will be nullified and you will have to restart the entire process.

Candidates must attain a score of at least 75 in order to pass each section with the lowest score being 0 and the highest being 99.

The three organizations you’ll have to know to take the CPA exam in the AICPA, Prometric, and your State Board. The AICPA develops the exam and writes the questions while Prometric administers the exam itself. Only your State Board approves and issues your CPA license, however.

Now that you have an overview of the exam process, let’s dive into how each CPA exam section is structured, formatted, tested, and scored.

CPA Exam Section Format & Structure

Each of the four CPA exam parts are structured into different testing blocks known as testlets.

AUD, FAR, and REG section consist of multiple choice questions (MCQs) and task-based simulations (TBSs) while BEC has MCQs, TBSs, and written communications in the weighted score.

Here’s a chart showing the CPA exam structure and distribution of task-based simulations and MCQs on each exam section.

| CPA Exam Section | Test Time Length & Duration | Multiple-choice Questions | Task-based Simulations | Written Communication |

|---|---|---|---|---|

| AUD | 4 hours | 72 | 8 | - |

| BEC | 4 hours | 62 | 4 | 3 |

| FAR | 4 hours | 66 | 8 | - |

| REG | 4 hours | 76 | 8 | - |

Let’s look at each testlet in detail, so you know what to expect on your exam day.

Multiple Choice Testlets

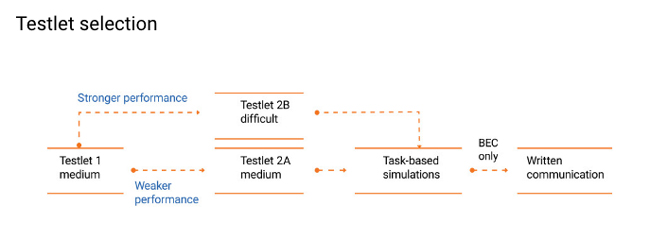

These are usually the favorite questions for most candidates. They may appear easy at first, but the truth is, they are sometimes tricky. By design, the first MCQs are usually of medium difficulty. Depending on how you answer them, you may encounter easier or more complex questions as you progress.

For example, if you get the medium MCQs testlet right, then the next testlet will be more complex. If you get it wrong, then the next testlet might be a bit easier.

Do not get excited to perform poorly on medium MCQs for hoping that the subsequent testlets will be easier. Instead, you must endeavor to answer each question accurately because weighting is not uniform. More complex MCQs carry more weight and will significantly contribute to the overall score compared to many easier questions.

Multiple choice questions can sometimes be confusing. To ensure that you make the right choices during the examinations, you must read and understand the question then quickly scan through the answers provided to eliminate wrong options. If a question is taking longer than expected flag and proceed to the next question but do not forget.

If you are unable to figure out the right answer, choose the closest option by your judgement. Never leave any question unanswered even if you are not sure about the answer. The rule of thumb here is that you must know the answer even before looking at the answers. Finally, allocate sufficient time to relook at the answers before submitting.

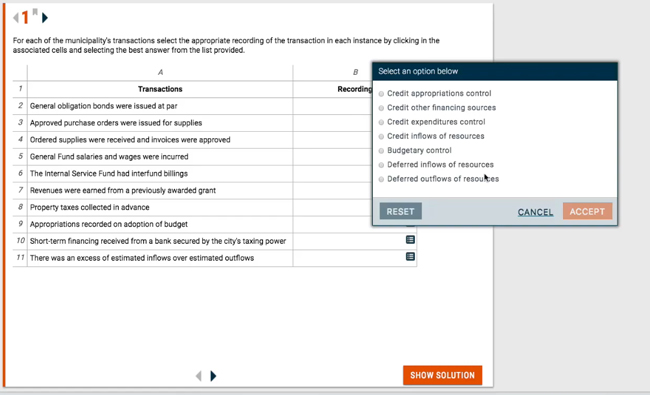

Task Based Simulations Testlets

The task-based simulation questions are designed to test your practical knowledge of different topics covered in specific CPA sections. Their formatting differs from MCQs and may require more time to answer them accurately.

They may involve matching concepts, document reviews, journal entries, or filling in blank spaces about real-life professional scenarios through critical thinking. You may also come across research-based questions requiring you to research and provide findings on specific topics in an exam.

You are likely to encounter about 6 or 7 task-based simulations questions for each of the four sections, and further broken down into three TBS testlets in REG, FAR, and AUD sections while BEC section has two TBS testlets. Simulations account for 50% of the exams AUD, FAR, and REG exams, and 35% of BEC.

The best way to pass TBS testlets is through extensive reading and revisions. You must understand the content of a typical CPA examination, practice with sample tests, understand the questions deeply, and know how to use supportive tools such as calculator, spreadsheets, and relevant literature.

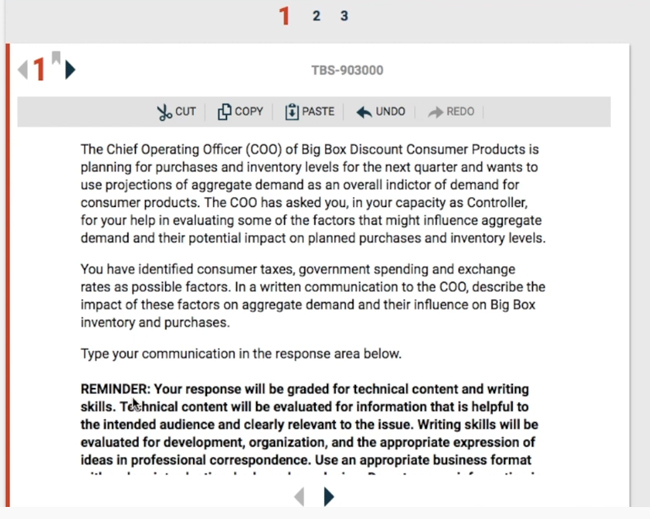

Written Communication Testlets

Communication is key in any profession, and accountancy is not an exception. Here, your communication skills and technical writing expertise are put to the test. You may be asked to draft an internal memo or a letter to a client.

Even though most candidates may find these testlets to be easy, you risk failing if you do not adhere to official formats or use unprofessional language or tone.

You will encounter written communication testlets in BEG exam and it accounts for 15% of the total score. Many candidates struggle with the written communication questions because their writing skills are not strong.

The best way to prepare for the written portion of the BEC section is to practice simulations in your CPA exam review guide. Most courses have several different written sample questions and answers that will help you get a feel for what the AICPA is looking for on the BEC section.

CPA Exam Section Scoring

The AICPA scoring process for the CPA exam is weighted evenly between multiple choice questions and task based simulations. This means that 50% of your score is based on how well you answered the MCQs. This can be good if you are a wizard at multiple-choice. It can also be a bad thing if you find simulations difficult.

It also means that simulations are more important. Since most of the sections have or less simulations, each one is worth a lot of points. You need to take practicing sims seriously! Keep in mind, the BEC exam is weighted slightly differently with 35% TBS and 15% written comms.

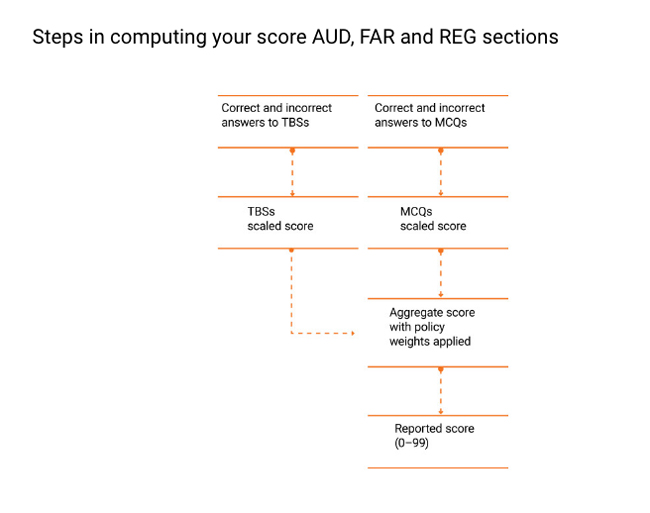

To determine the total score for AUD, REG, and FAR, AICPA weighs the scores attained in task-based simulations (TBSs) and multiple-choice questions (MCQs), each accounting for 50%.

| CPA Exam Section | Multiple-choice Questions (MCQs) | Task-based Simulations (TBSs) | Written Communication |

|---|---|---|---|

| AUD | 50% | 50% | - |

| BEC | 50% | 35% | 15% |

| FAR | 50% | 50% | - |

| REG | 50% | 50% | - |

Here are the steps to score/grade your Audit, Financial Reporting, and Regulations exam sections:

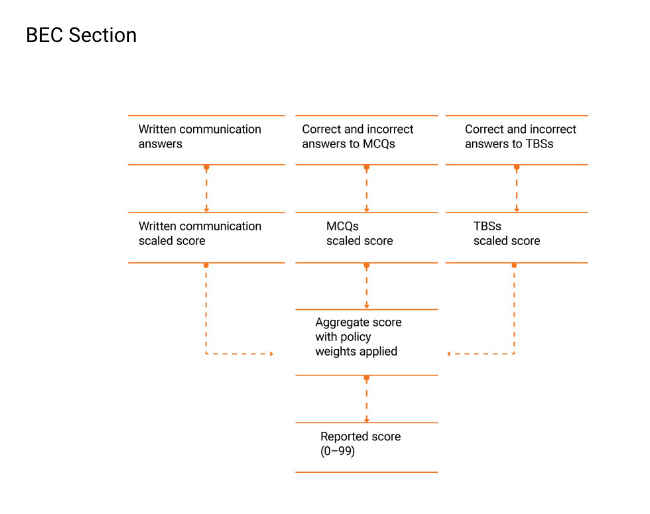

This is not the case with the BEC section, where the total score is determined by the scores attained in MCQs (50%), TBSs (35%) and written communication (15%).

Here are the steps to score/grade your BEC exam section:

CPA Exam Section Topics & Content Area

Each section of the CPA exam covers different topics and is graded slightly differently. Let’s look at the distribution of topics and the specific percentages across each section that you will encounter on your exam.

Auditing and Attestation (AUD)

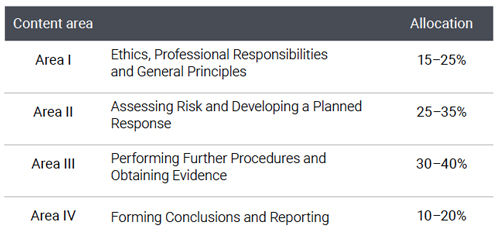

AUD focuses on four areas: ethics and professional responsibilities, performing audit procedures and obtaining evidence, assessing risk, and developing a planned response, and developing conclusions and reports. This section will test the candidate’s evaluation skills. The exam usually takes four hours, consisting of 72 MCQs, and 8 TBSs.

Here are the topics tested on the AUD exam:

- 15%-25% on ethics and professional responsibilities

- 30%-40% on performing audit procedures and acquiring evidence

- 20%-30% on assessing risk, and formulating a response

- 15%-25% on developing conclusions and reports

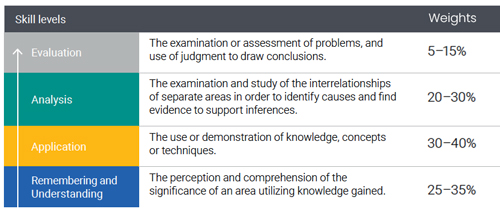

The AUD CPA exam section is designed to test CPA candidates’ higher order skills. The AICPA has identified four different levels of skills that are critical to master in order to pass the Auditing section. Here is a detailed look at the AUD exam skill allocations and their weights.

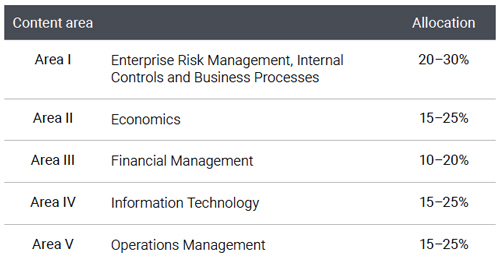

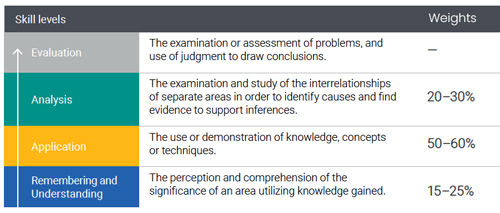

Business Environment and Concepts (BEC)

BEC tests the candidate’s competence in conducting the day-to-day work-related tasks. It covers five topics: corporate governance, financial management, economic concepts and analysis, operations management, and information technology.

Here is the content covered on the BEC exam:

- 15%-25%: Operations management

- 15%-25%: information technology

- 17%-27%: Economic concepts and analysis

- 17%-27%: Corporate governance

- 11%-21%: Fiscal management

The BEC CPA exam section was developed to test CPA candidates’ application skills mainly focusing on business concepts that would be useful to deploy in the real world. Understanding how a business profit centers work and the economics of business is key to pass the Business Environment section. Here’s more details of the BEC exam skill allocations and their weights.

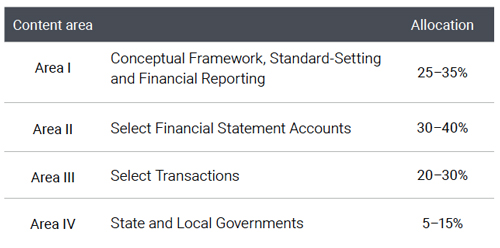

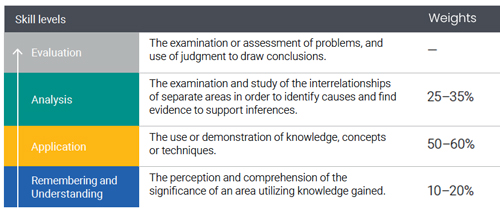

Financial Accounting and Reporting (FAR)

FAR focuses on testing the suitability of the candidate to competently execute this mandate. The topics you will encounter will include conceptual framework, financial reporting and standard setting, financial statement preparations, financial transactions in line with US GAAP and IFRS rules, and compliance with state and local governments.

Here’s the distribution of topics tested on the FAR exam:

- 5%-15%: State and local government

- 20%-30%: Select financial transactions

- 30%-40%: Financial statement account

- 25%-35%: Financial reporting and conceptual framework

The FAR CPA exam section was created to test CPA candidates’ application skills of financial accounting. Being able to apply your knowledge of financial reporting in real world situations is a big part of passing the Financial Accounting section. Here’s how the FAR section skill levels are weighted.

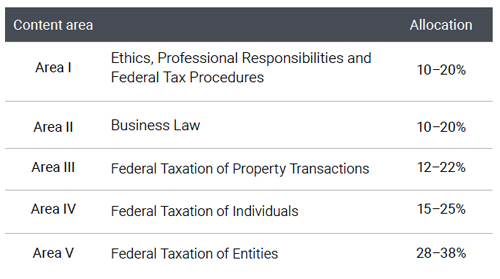

Regulation (REG)

Unlike the first three sections of CPA, REG does not focus explicitly on accounting. Instead, it dwells more on issues around taxation, business laws, ethics and professional conduct, and procedures.

Below is a rundown of the content and percentages tested on the REG exam:

- 28-35%: Federal taxation of entities

- 15%-25%: Individual federal taxation

- 12%-22%: Federal taxation and property transactions

- 10%-20%: Business law

- 10%-20%: Ethics, professional responsibilities, and federal tax procedures

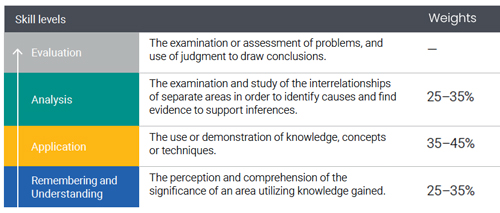

The REG CPA exam section tests 3 out of 4 higher order skills. The AICPA wants to make sure you can understand, analyze, and apply legal and tax topics in business situations. Here are the weights of each skill level tested on the REG section.

CPA Exam Sections Ranked Hardest to Easiest

According to the AICPA published CPA exam pass rates, the four CPA exam sections ranked from hardest to easiest are as follows:

- FAR

- AUD

- REG

- BEC

Most CPA candidates consider FAR to be the hardest CPA exam section while BEC is the easiest. This is partly to do with the length and vast amount of content that FAR covers. FAR is the longest exam section and covers the most topics. It’s difficult for candidates to memorize this many facts and topics for a single exam.

Likewise, BEC is the shortest exam that covers the least amount of specialized topics. BEC also includes a written simulation that doesn’t involved memorizing facts or studying. It merely tests your ability to write and communicate clearly.

REG consistently ranks as the second easiest exam while AUD ranks the second hardest CPA exam. These rankings show that candidates struggle more with auditing procedural topics than law and taxation concepts. Since auditing is vary specialized, it does make sense that candidates would struggle with that more.

Frequently Asked Questions

Here are some of the most commonly asked questions about the sections of the CPA exam.

What are the 4 parts of the CPA exam?

The four parts of the CPA exam are AUD, BEC, FAR, and REG. Each exam section tests a candidates ability to understanding accounting topics and apply them in real world scenarios.

What are the CPA sections in order of difficulty?

Most CPA candidates agree that FAR is the hardest CPA exam section followed by REG, AUD, and BEC. Typically, BEC is considered the easiest because of its short length and written simulation.

What is the CPA exam tax section?

Regulations (REG) is the section of the CPA exam that tests candidates’ knowledge of taxation, business law, and economics. The exam part relies heavily on memorizing tax codes and legal cases to answer multiple choice questions.